Tertiary study

Eligible fees, course costs, equipment and approved transition expenses, subject to Stage 0 rules.

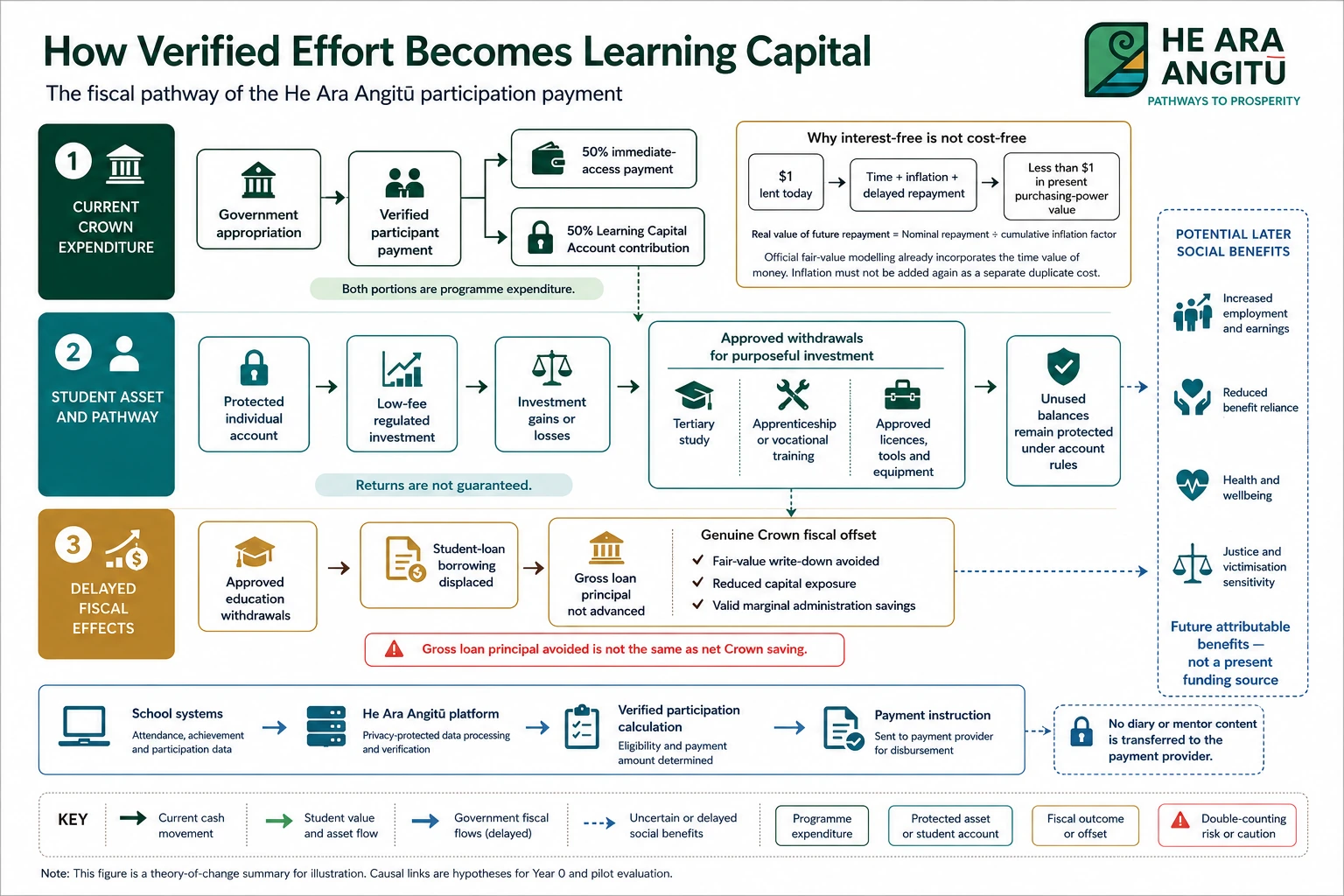

Learning Capital is the protected portion of verified participation support. Its purpose is to help fund approved tertiary, vocational and apprenticeship pathways—not to manufacture a fiscal saving by counting the same dollar twice.

Under the current model, half of verified participation payments would remain immediately accessible and half would be placed into protected Learning Capital.

Over five school years, central modelled protected contributions total approximately $9,750 per participant. The projected nominal closing balance is approximately $10,682, after investment, fees, tax and lifecycle assumptions.

Eligible fees, course costs, equipment and approved transition expenses, subject to Stage 0 rules.

Industry training, tools, licences, safety equipment and recognised vocational costs.

Approved training and entry costs that help a participant begin and complete a durable pathway.

Stage 0 must determine whether any additional uses are justified, how hardship access works, what happens when a participant changes direction, and how unused balances are treated.

No employer owns the account, no provider gets exclusive access, and no political office gets to quietly repurpose it.

Low fees, prudent investment, transparent statements, clear complaints and independent oversight.

The resource follows the participant across approved pathways rather than trapping them inside a sector’s recruitment plan.

The same dollar is not allowed to enter the benefits column as account value, debt avoided, Crown saving and social return four times while hoping nobody recognises it.

Who owns the assets, who is the trustee and what protections apply?

Which costs qualify and how are unusual circumstances handled?

What risk settings, fees, tax treatment and lifecycle options are appropriate?

How do students with interrupted participation, disability or severe hardship avoid being penalised twice?

How much student borrowing is genuinely displaced rather than simply accompanied?